Roll over image to zoom in

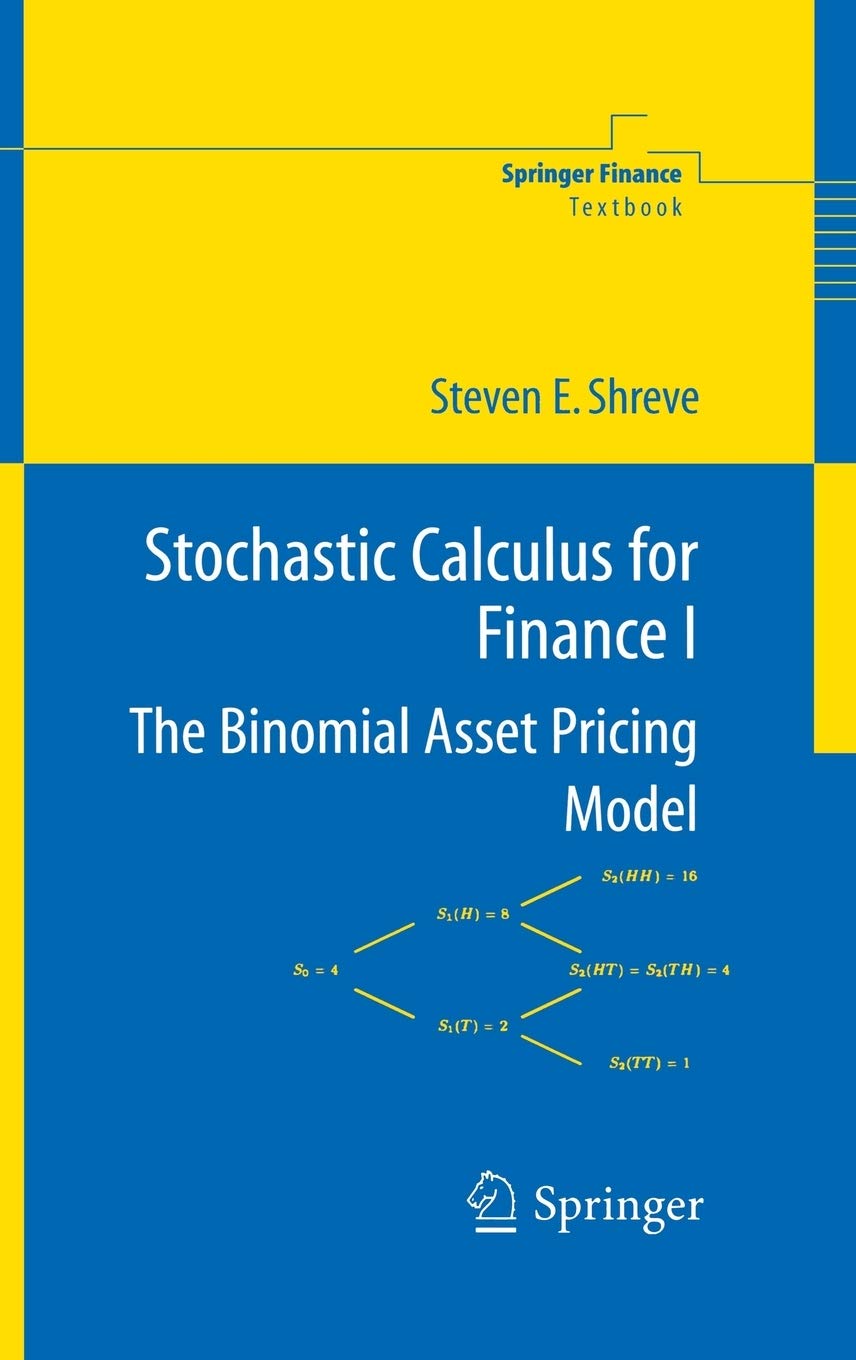

Stochastic Calculus for Finance I: The Binomial Asset Pricing Model (Springer Finance)

£46.90

Developed for the professional Master’s program in Computational Finance at Carnegie Mellon, the leading financial engineering program in the U.S.

Has been tested in the classroom and revised over a period of several years

Exercises conclude every chapter; some of these extend the theory while others are drawn from practical problems in quantitative finance

Read more

Additional information

| Publisher | 2004th edition (21 April 2004), Springer |

|---|---|

| Language | English |

| Paperback | 202 pages |

| ISBN-10 | 0387401008 |

| ISBN-13 | 978-0387401003 |

| Dimensions | 15.49 x 1.19 x 23.5 cm |

by paul zhao

great

by QAguy

Great book in a great condition

by snowave

chapter 1-5 is well written, with very clear analysis along with proofs. chapter 6 is a bit ambiguous on descriptions about forward price and forward interest rates. some times these two concepts are described in a mixed manner,which make me confused..

by Tahir Usman

I purchased this for my sister, who required this for her Maths degree. Not much else to say really, I presume it was one of the recommended texts and she did well in her exams!

by Lence

A nice introduction into derivative pricing for someone with no experience in finance (like myself). A good introduction/foundation before moving onto continuous models.

by ian

nice and structured content, suitable depth (for me with an engineering background,no financial experience before) and it’s a very good reference book as well.

by Klau

I wish it described in more details it’s steps but if you spend more time on it, you’ll understand it well.

by siti ali

very useful to math students. easy to understand. got good examples. got exercises with detailed solutions. recommended to all. thanks